Topics on this page: Audit Enforcement and Risk Oversight | What Is a Single Audit? | Audit Submission Requirements | About the Audit Resolution Division | How to Submit HHS Single Audit Reports | Delinquent Audit Reports | Audit Report Extensions | What’s New | Helpful Resources

Audit Enforcement and Risk Oversight (AERO)

HHS has launched the Audit Enforcement and Risk Oversight (AERO) initiative, a department-wide program integrity effort to address persistent Single Audit noncompliance among states and grantees.

AERO will strengthen grant oversight by improving consistency, transparency, and documentation; increasing visibility into unresolved audit findings; enhancing coordination across HHS; and setting clearer expectations for timely corrective action and enforcement follow-through. The initiative reflects HHS’s commitment to working with states and grantees to resolve issues early, strengthen internal controls, and protect taxpayer dollars.

Please contact AuditResolution@hhs.gov with any questions or concerns.

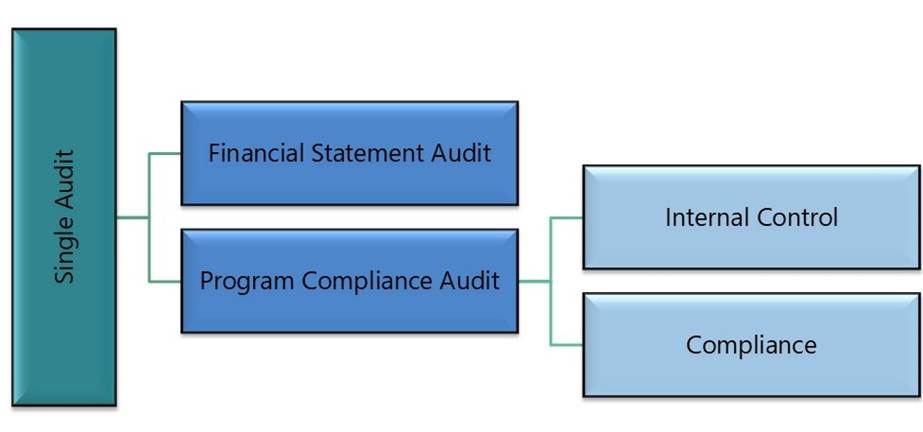

What Is Single Audit?

Under 2 CFR Part 200 (Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, also known as the Uniform Guidance) and the [Single Audit Act of 1984 (as amended in 1996)], any non-Federal entity (i.e., award recipient) that expends $1,000,000 or more in Federal financial assistance during its fiscal year is required to undergo a Single Audit. As shown in Figure 1, a single audit includes a financial statement audit and a program compliance audit.

Figure 1: Single Audit Components

A single auditor selects a recipient’s Federal program(s) for a compliance audit based on the Federal awards dollars expended, program risk level, and other considerations. The audit findings may include deficiencies in internal controls or noncompliance in areas such as:

- Allowable costs or activities

- Eligibility

- Timeliness of required reporting

- Other Federal compliance requirements

Audit Submission Requirements

The Uniform Guidance requires recipients to must submit their Audit Reporting Package to the Federal Audit Clearinghouse (FAC) no later than:

- 30 days after receipt of the auditor’s report, or

- 9 months after the fiscal year end, whichever comes first

Federal awarding agencies are required to issue management decisions within six months of the FAC’s acceptance of the audit report.

About the Audit Resolution Division

The HHS Audit Resolution Division (ARD) oversees the resolution of audit findings related to HHS programs and operations. The Division ensures that discrepancies, compliance issues, and non-conformities identified through audits are properly addressed and corrected.

Our Responsibilities

- Audit Findings Resolution

- Analyze Single Audit findings affecting multiple HHS Divisions to support effective and timely resolution.

- Management Decisions (MDLs)

- Ensure the timely issuance of Management Decision Letters (MDLs) in accordance with federal requirements.

- Questioned Costs Oversight

- Monitor and ensure appropriate management actions are taken to resolve questioned costs, including corrective actions and cost recovery, where applicable.

- Delinquent Audit Monitoring

- Track overdue Single Audit submissions and coordinate follow-up with HHS Divisions and recipients.

- Regulatory Compliance

- Promote adherence to federal guidelines and audit requirements.

- Standard Operating Procedures

- Enhance the efficiency and consistency of HHS Single Audit resolution efforts through structured protocols.

- Interagency Coordination

- Collaborate with federal partners to strengthen audit resolution strategies.

For questions about Single Audit, please send them to AuditResolution@hhs.gov.

Submission of HHS Single Audit Reports

- Non-Profit Entities:

Submit reports to the FAC - For-Profit Entities:

Submit reports to: For-Profit_Audit@hhs.gov - Foreign Entities:

- Except CDC awards: Foreign_Audit@hhs.gov

- CDC awards: ormic.audit.resolution@cdc.gov

Delinquent Single Audit Report Submission

An audit reports is considered delinquent if not submitted by the earlier of:

- 30 days after receipt of the audit report, or

- 9 months after fiscal year-end.

Single Audit Report Extension

Due date extensions are granted only under specific, extraordinary circumstances, such as:

- Declared national disasters or public health emergencies

- Systemic technical issues with the FAC

- Widespread external events affecting many auditees

For additional or clarifying questions about Single Audit extensions, please send them to Single_Audit_Extension@hhs.gov.

What’s New

Single Audit Report Extensions for Hurricane Helene, Hurricane Milton, and the California Wildfires

Resources

- CDC FAQ on Audits for Foreign-Based Entities

- Centers for Medicare & Medicaid Services

- Council on Federal Financial Assistance (COFFA)

- Health Resources & Services Administration

- HHS Office of Inspector General

- Title 2 Code of Federal Regulations Part 200

- Government Auditing Standards

- Office of Management and Budget Circular A-133 Compliance Supplements

- Single Audit Act of 1984 (as amended in 1996)